Leadership Transition & Change

Succession Planning When You ARE the Whole Business

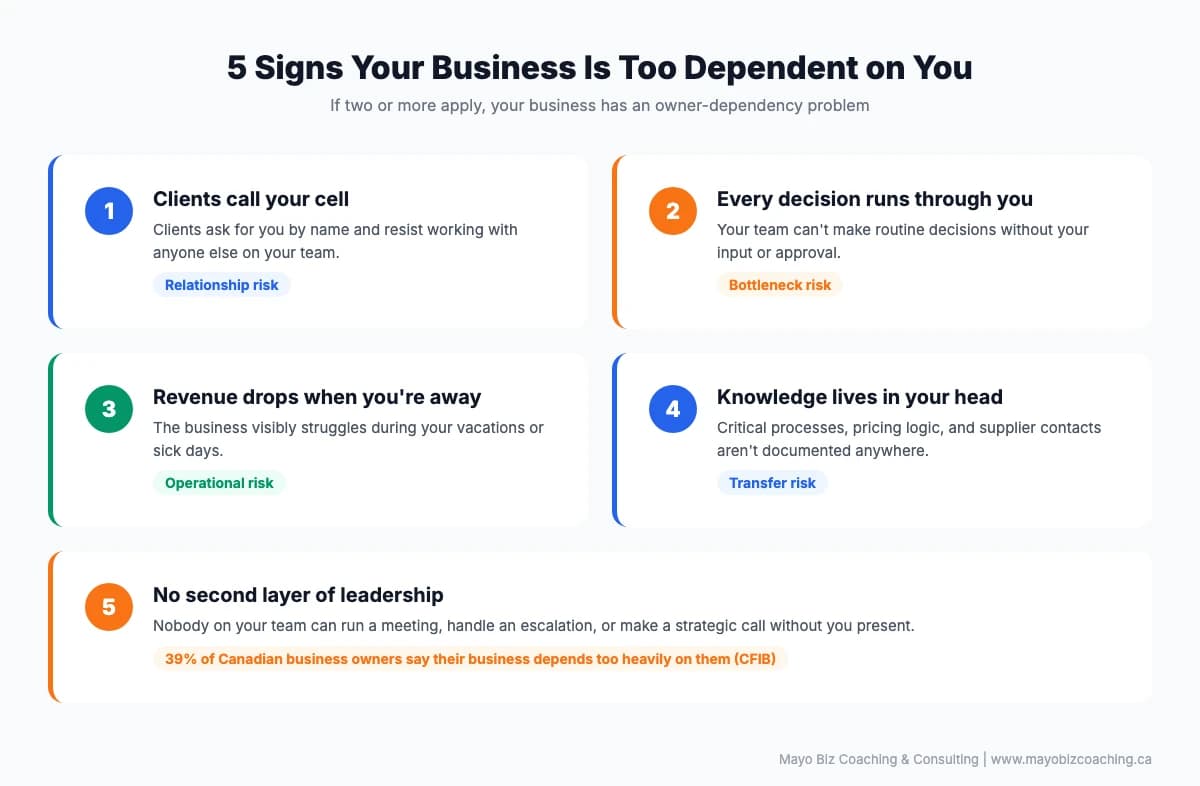

Your clients call your cell phone. Your team checks with you before making decisions they could handle on their own. The biggest deals close because of your relationships, not the company's reputation. If you disappeared for three months, would the business keep running? Or would it stall?

For most small business owners, the answer is hard to hear. You are the business. And that makes succession planning a different conversation entirely.

The Succession Crisis Nobody Is Ready For

In a 2023 survey 1, the Canadian Federation of Independent Business (CFIB) found that 76% of small business owners plan to exit their business within the next decade. That puts over $2 trillion in business assets in play across Canada. Only 9% have a formal succession plan.

In coaching, I see why that gap exists. Succession planning feels like something for later. You're still running the business, still growing it, still putting out fires. Retirement is a vague idea somewhere on the horizon.

But "later" has a way of arriving faster than expected. The same CFIB survey found that 22% of owners are already burned out and 21% want to step back from their responsibilities. The exit may come sooner than you planned.

The gap between wanting to leave and being ready to leave is where most owners get stuck.

Why Owner-Dependent Businesses Are Harder to Transfer

Buyers don't want to buy you. They want to buy a business that works without you.

Nearly four in ten owners will tell you their business can't function without them. The CFIB confirmed this in their 2023 succession report 2 (see full report PDF), putting the number at 39%. And 54% say finding a suitable buyer or successor is their biggest obstacle.

These two problems are connected. When the owner holds all the client relationships and makes every decision, the business has no transferable value beyond its assets. A buyer looks at that and sees risk. They're not buying a company. They're buying a job.

I've watched this play out with clients who spent years building something valuable, only to discover that the value walked out the door with them. Industry estimates suggest that roughly 70% of small businesses never successfully sell 3, and owner dependency is the primary driver.

What a buyer wants to see is a business that runs on systems, relationships, and capable people. Not one that runs on a single person's presence.

The Identity Problem

The real reason succession planning stalls isn't finances or paperwork. It's identity.

When you built the business from nothing, your identity became inseparable from it. You're the one closing deals and solving problems. You're the face of the brand. Over years of 60-hour weeks, the line between who you are and what the business is disappeared. Stepping away doesn't just mean leaving a company. It means letting go of the thing that defines you professionally and personally.

For many owners, that redefinition is more frightening than the financial uncertainty of retirement.

I worked with one owner who had a solid operations manager ready to take over client calls. Every Monday, he'd say "this is the week I step back." By Wednesday, he'd be on the phone with his three biggest accounts "just to check in." When I asked him why, he said, "If I'm not talking to clients, what exactly do I do here?" That question is the real obstacle.

Each reason to stay involved is valid on its own. Together, they form a pattern: the owner can't let go because letting go means answering a question about who they are without the business.

This is the same identity challenge I wrote about in from operator to leader. The shift from doing the work to building the people who do the work means changing how you see yourself. Succession planning goes further. You're preparing the business to exist without you entirely.

The hardest part of succession planning isn't the paperwork. It's accepting that the business needs to outgrow you.

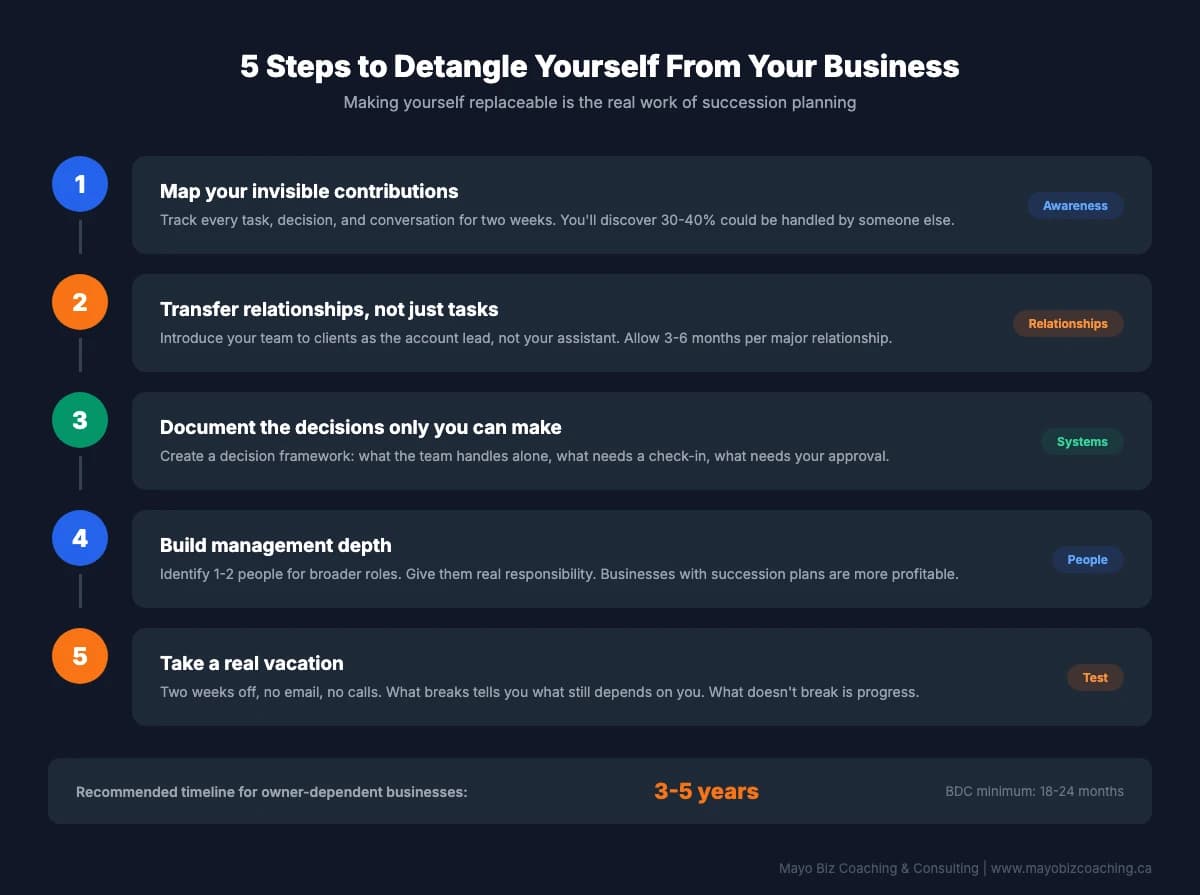

Five Steps to Detangle Yourself From the Business

Succession planning for owner-dependent businesses isn't about writing a will or setting a sale price. Those come later. The real work is making yourself replaceable. Here is how.

1. Map your invisible contributions

Most owners underestimate how much they do that nobody else sees. Start by tracking every task, decision, and conversation you handle for two weeks. Include the things that feel too small to mention: the supplier you call when inventory is late, the client you smooth things over with, the employee conflict you mediate informally. Write all of it down.

In my experience, owners typically discover that 30 to 40% of what they do could be handled by someone else with the right training and authority. Another 20% could be systematized. The remaining work is where your time should actually go.

2. Transfer relationships, not just responsibilities

This is where most delegation frameworks fall short. Handing off tasks is only half of it. The harder part is handing off relationships.

Start introducing your team to major clients, suppliers, and partners. Not as your assistant. As the person who handles their account. Sit in on meetings together at first, then let your team member lead while you observe. Eventually, step out entirely. In my experience, this transition takes three to six months per important relationship.

The goal is for the client to trust the person, not just the business through you. For a detailed approach to handing off work without losing quality, the delegation without abdication framework walks through this step by step.

3. Document the decisions only you can make

Every business has a handful of decisions that genuinely require the owner's judgment: pricing strategy, major contracts, senior hires, financial commitments above a certain threshold. These are legitimate owner decisions.

But most owners also make dozens of decisions daily that don't require their involvement at all. A team member asks about a routine client request. Someone checks whether to order supplies. An employee wants approval for a schedule change. Each interruption takes five minutes. Together, they consume hours.

Create a simple decision guide and put it in writing:

- What your team can handle without asking

- What needs a quick check-in

- What genuinely needs your approval

Then enforce it by not answering the questions that fall into the first category.

4. Build management depth

A business that depends on one person is a business with no management depth. If you're the only one who can lead a team meeting, handle a client escalation, or make a strategic call, the business has a single point of failure.

Start developing your next layer of leadership now. Identify one or two people who could step into broader roles. Give them real responsibility, not busywork. Let them make mistakes and learn from them.

A 2025 Gallup survey of U.S. small business owners 4 found that businesses with long-term succession plans tend to be larger and more profitable. That's not a coincidence. Owners who invest in their people build businesses that grow beyond their personal capacity.

5. Take a real vacation

This sounds trivial. It isn't. Take two weeks off without checking email, without taking calls, without "just quickly" responding to a message. Tell your team they need to handle everything.

What breaks while you're gone tells you exactly what still depends on you. What doesn't break proves that your team is more capable than you think. Both pieces of information are valuable.

One client came back from two weeks away to find that his warehouse team had solved a recurring shipping problem he'd been personally managing for years. They just needed the space to figure it out. Another came back to three upset clients because nobody on staff had the authority to approve a routine change order. Both results gave them a clear picture of what to work on next.

If you can't take two weeks off without the business suffering, that's your succession plan talking.

When to Start Succession Planning

The BDC recommends starting succession planning at least 18 to 24 months 5 before your desired exit. For owner-dependent businesses, that timeline is too short. If the business is built around you, you need three to five years of deliberate work to detangle yourself.

That sounds like a long time. But consider what has to happen in that window. Transferring client relationships, developing leaders, and getting institutional knowledge out of your head all take longer than owners expect.

You also need to prove, to yourself and to a buyer, that the business runs without you. None of that happens quickly.

The owners who start early have options. They can choose their buyer, negotiate from strength, and transition gradually. Owners who wait for burnout, a health scare, or a market shift end up with fewer options and worse terms.

This framework assumes you have people to develop and relationships worth transferring. Not every business does. Some owner-dependent businesses are too small or too specialized to build a second layer of leadership. That's worth being honest about early, because it changes whether your exit looks like a sale, a merger, or a planned wind-down.

Selling isn't the only valid exit. Some owners choose a planned wind-down because the cost of detangling exceeds the expected sale value. That's a legitimate choice. But even a wind-down goes better when the business isn't entirely dependent on one person.

The CFIB found that 90% of owners prioritize protecting their employees when they sell. That's a good instinct. But you can only protect your people if the business is strong enough to survive the transition. And that strength comes from years of preparation, not a last-minute plan.

The Conversation Most Owners Avoid

There's a question I ask owners in coaching that usually gets silence: "If you got hit by a bus tomorrow, what happens to the business?"

Most owners don't have a good answer. The business would struggle. Clients would leave. Institutional knowledge would be lost. The team would flounder without direction.

That's not a succession plan. That's a vulnerability.

You don't have to sell the business tomorrow. You don't have to retire next year. But you do need to start building a business that can stand on its own. Build it to run without you, not as an exit strategy, but because that's what a healthy business looks like.

If you're carrying all of it right now, that's usually what brings owners to coaching. Addressing it is worth doing on its own, well before any exit is on the table. If burnout is already part of the picture, understanding why it's a leadership problem is a good place to start.

This article reflects coaching experience and is educational in nature. It is not a substitute for professional legal, financial, or accounting advice. Work with qualified advisors for decisions about selling, transferring, or valuing your business.

Start Building a Business That Runs Without You

Succession planning doesn't start with lawyers and accountants. It starts with building a business that works without you in the middle of everything.

If you're recognizing that your business depends too heavily on you and you want to change that, reach out for a free consultation. No sales pitch, just an honest conversation about where you are and what you're working on.

Research Notes & Sources

If you want to go deeper, these are the studies and reports behind the key points in this post.

- Over $2 trillion in business assets are at stake as majority of small business owners plan to exit their business over the next decade(cfib-fcei.ca)

- Succession Tsunami: Preparing for a decade of small business transitions in Canada(cfib-fcei.ca)

- 20 Key Business Owner Statistics on Exits & Succession(project-equity.org)

- Most Small-Business Owners Lack a Succession Plan(news.gallup.com)

- How to create a succession plan(bdc.ca)

Category & Tags

Frequently Asked Questions

When should a small business owner start succession planning?

Start at least three to five years before you want to step away. The BDC recommends a minimum of 18 to 24 months, but owner-dependent businesses need longer because detangling yourself from daily operations takes time most owners underestimate.

Why do most small businesses fail to sell?

Roughly 70% of small businesses never find a buyer, mostly because of owner dependency. When the business cannot function without the founder, buyers see risk instead of value. Reducing that dependency is the single biggest thing you can do to make your business sellable.

How do I know if my business is too dependent on me?

Three signs: clients ask for you by name and resist working with anyone else, your team cannot make routine decisions without your input, and revenue drops noticeably when you take time off. If any of these are true, the business is built around you, not around systems.

What is the difference between an exit plan and a succession plan?

An exit plan is your personal timeline and financial goals for leaving. A succession plan is the operational work of building the business so it runs without you. Most owners focus on the exit plan and skip the harder succession work, which is why so many businesses fail to transfer.

About the Author

About the Author

Mark Mayo

Head Coach, MBC

We get up each morning excited about sharing our 20-plus years of business acumen with small business owners and their teams. Collaborating with hard-working owners to achieve their personal and business goals brings rewards. When we develop you and grow your leaders, we create the momentum that moves you and your business forward. It starts with a first step. Then we can build brilliance together.

Related Articles

From Operator to Leader: How Business Owners Make the Shift

Most owners started their business by being great at the work. That same hands-on identity becomes the ceiling. Five shifts to move from operator to leader.

Read From Operator to Leader: How Business Owners Make the Shift

Ghost Growth: The Fake Promotions Driving Your Team Away

Ghost growth gives employees titles without real advancement. Learn why fake promotions backfire and what leaders can do instead to retain talent.

Read Ghost Growth: The Fake Promotions Driving Your Team Away

The First 90 Days: How a Coach Helps You Succeed in a New Role

McKinsey research shows coaching doubles the success rate for leaders in transition. A practical 90-day framework to reach effectiveness faster.

Read The First 90 Days: How a Coach Helps You Succeed in a New Role